The government has set an ambitious aspirational goal of India becoming a developed country by 2047. Then there are formidable international commitments to contribute towards achieving global public good—net zero GHG (greenhouse gas) emissions by 2070; and before that by 2030 reduce emissions intensity of its GDP to 45% from 2005 level, and achieve 50% cumulative electric power installed capacity from non-fossil fuel-based energy sources. Along this sustainable development journey, rapid technological changes pose additional challenges and opportunities.

The level of actual achievements vis-à-vis envisaged goals and commitments would critically depend on the right financing model to fund the required schemes and projects.

The Indian economy is bank-dominated. Going forward, the banks would need to continue to play their important role. That said, bank financing of projects has its limitations. The build-up of banks’ humungous non-performing assets (NPAs) on account of reckless funding of infrastructure projects during 2009-2013 made everyone realize that the banks are not best suited to fund long gestation projects on account of the potential asset-liability mismatch problem. Not only the infrastructure projects required to make India a developed country but also many of the green and transition projects fall in the long gestation period category, with back-ended returns. The capital markets, with their various instruments, provide a good financing option for such projects.

The good news is that the capital markets in India have come of age. Today, India can rightly boast of having one of the best-in-class securities market regulatory architecture. This has been well demonstrated in the last few years, wherein a series of major global events roiled the world financial markets. In this tumultuous period, the robustness of the Indian capital markets and their performance, as compared to the peers as well as developed economies of the West, have clearly stood out. The Indian markets, with market capitalization crossing $5 trillion, are now ranked fourth in the world in terms of size, behind the US, China and Japan. The market cap to GDP ratio recently crossed 150%.

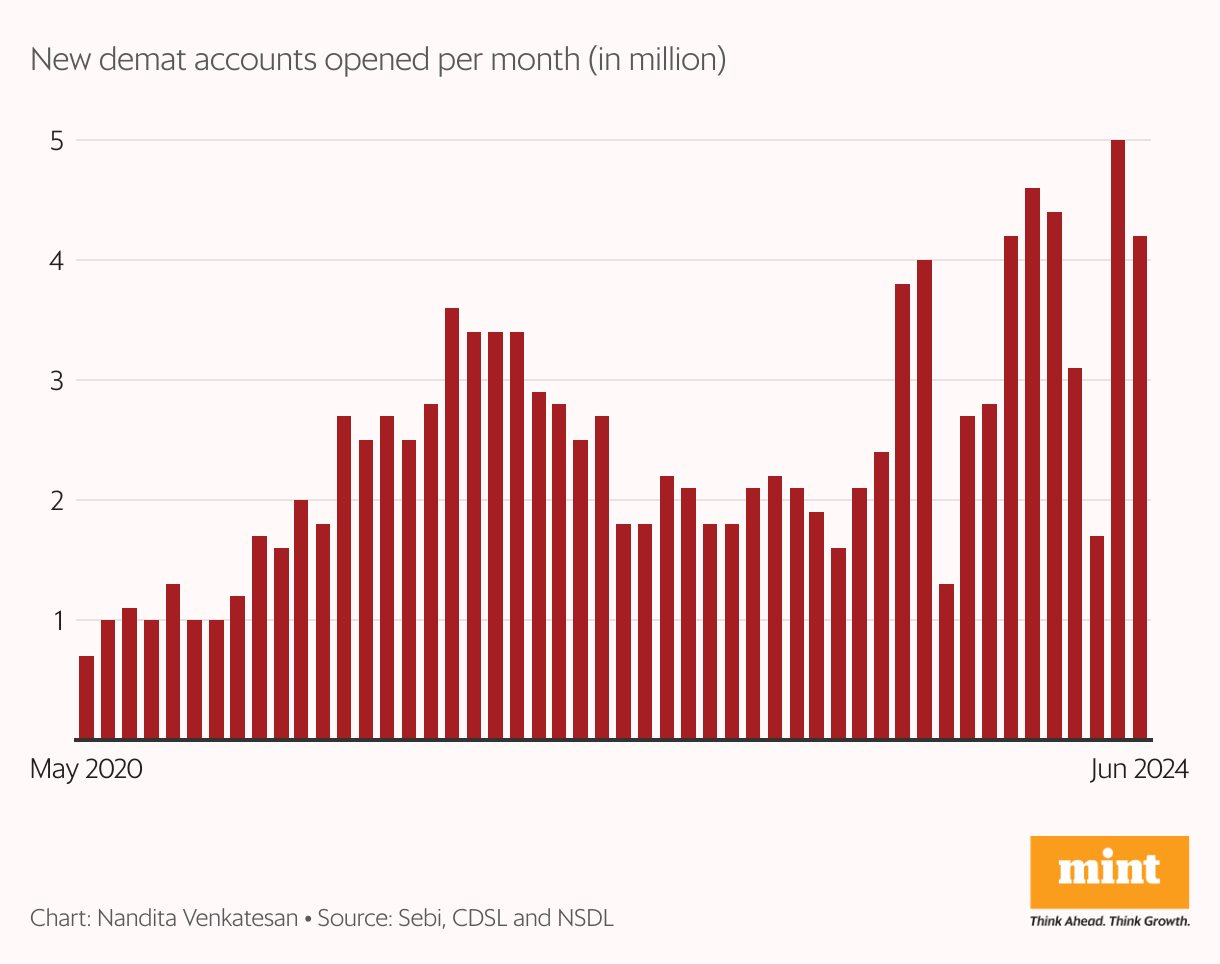

The marked increase in investment by domestic investors, especially retail investors, in the last few years has added to market resilience, making it less vulnerable to capital outflow shocks. The total number of demat accounts increased from 41 million in March 2020 to over 160 million at present, an increase of over 290% in a short period.

This must be sustained and encouraged with a view to facilitating people’s participation in wealth creation.

As for the changes in technology, the Indian capital markets are well-placed to meet the challenges and harness the opportunities. The regulator, market infrastructure institutions and market participants are tech-savvy, and quick to learn and adapt. The ease with which they have assimilated the usage of artificial intelligence (AI) and machine learning (ML) in their functioning and operations is remarkable.

It would thus be fair to deduce that the equities markets are well placed to serve India in its quest to become a developed country in the coming decades.

In addition to the equities, the framework for hybrid instruments such as infrastructure investment trusts (InvITs) and real estate investment trusts (Reits), though of recent origin, has rather come out well. Some regulatory improvements are on the anvil, and some more could follow later as the market matures. These instruments are of particular help in monetizing the brownfield infrastructure and real estate projects. The freed capital could then be used to finance new projects. These instruments are poised to play an important role in India’s growth story in the coming years.

The elephant in the room is the underdeveloped corporate bond market in India, requiring priority attention of the government.

India’s aspirations to become a developed country need to be backed by a liquid, deep, and well-functioning debt market—something that the country does not have. An efficient Indian corporate bonds market with lower costs and faster issuances could provide a cost-effective source of long-term finance to Indian corporates. While some recent regulatory changes have improved the ease of doing business, helped increase transparency in the primary market, and enhanced liquidity in the secondary market, more reforms are needed. The most desirable one being the unification of the bond market, i.e., the unification of the regulatory regime for G-Secs, or government securities, and corporate bonds for both issuance and trading. This would significantly simplify the processes for investors, traders, and other stakeholders. G-Sec is like any other security and should be treated like one; having a separate regulatory regime for it is counter-productive. The setting up of a credible credit enhancement mechanism and the development of markets for credit default swaps (CDSs) and interest rate derivatives are other important asks.

A developed bond market is also a prerequisite to meet the debt requirements of green and energy transition projects. These projects are likely to need a substantial proportion of foreign funding in the foreseeable future. At least two essential steps need to be taken to facilitate this. The government should come out with a comprehensive and unambiguous taxonomy on what is to be considered as ‘green’ investment, and the RBI should deepen the domestic currency hedging market to reduce hedging costs.

Much work needs to be done to revamp the urban infrastructure in the country. As per an estimate, about 800 million people are likely to live in urban areas by 2050. Most municipalities in India are resource-starved and face an uphill task in raising funds for their development projects. The market regulator had come out with the municipal bond regulations in 2015 and many modifications have been brought therein, from time to time, in consultation with stakeholders. Unfortunately, this instrument is yet to gain popularity. Till now, only 14 issues of municipal bonds have been made, raising a rather small amount of about ₹2,400 crore. The municipalities need handholding and guidance, not only from the regulator but also from the central and state governments.

Lastly, there is a need for Indian corporates to improve their governance practices; though, admittedly, progress has been made over the period because of constant prodding by the government and the regulators. That said, Indian corporates need to do much soul searching and demonstrate responsible behaviour towards not only shareholders but also all stakeholders. Going forward, they ought to be also prepared to meet the increasing regulatory requirements of sustainability and climate-related disclosures.

Ajay Tyagi, formerly in the Indian Administrative Service, was chairman of the Securities and Exchange Board of India and is a distinguished fellow at the Observer Research Foundation.